Gen Z – A Recipe for Benefits

By: Sara Rubinstein

We all love burritos, and we all love benefits. So when I saw a press release from Chipotle to hire more Gen Z employees[1], it had me wondering: Is Chipotle offering the right benefits for Gen Z?

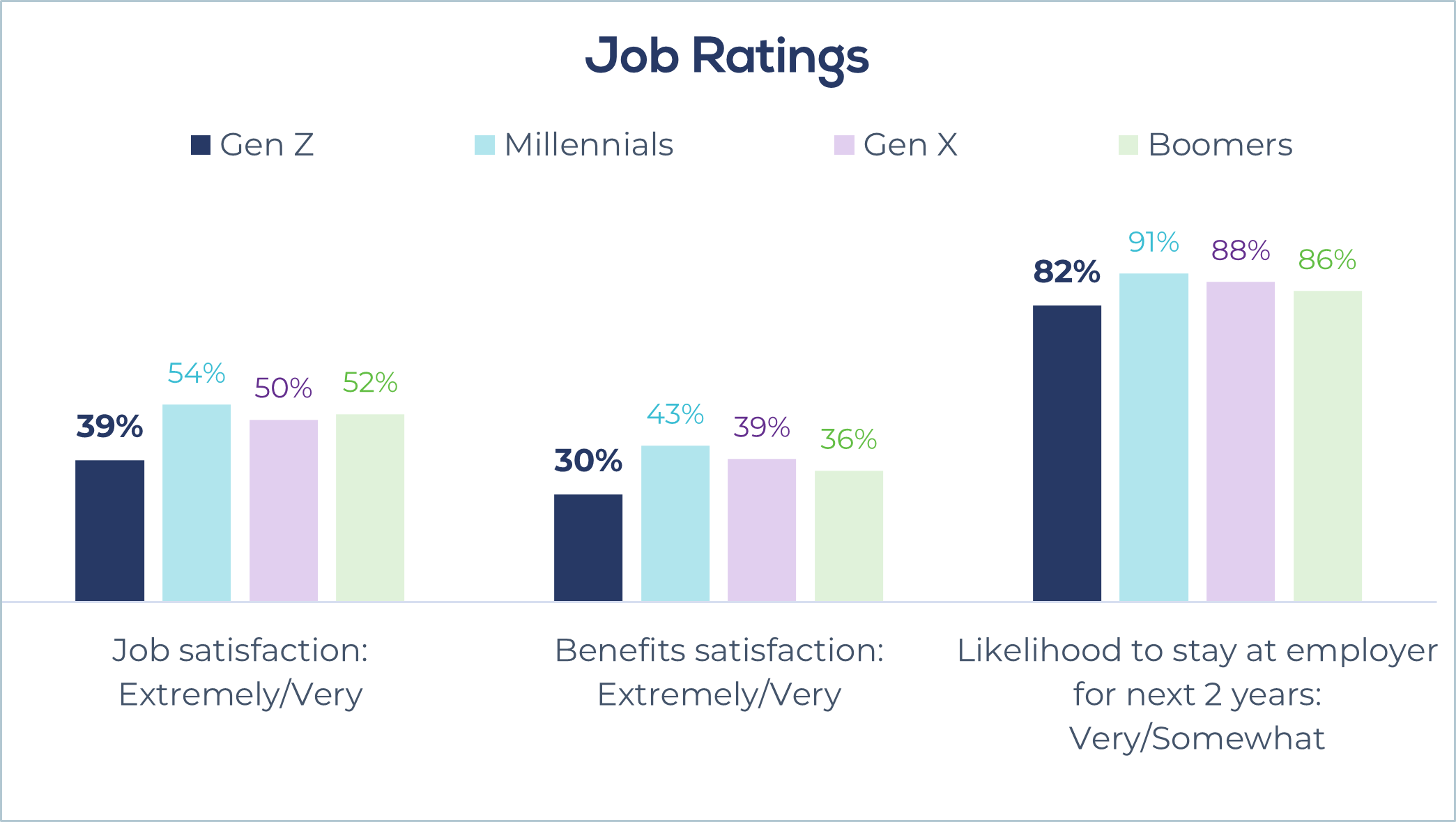

According to the 2023 EBRI/Greenwald Workplace Wellness Survey, Gen Z employees, defined as those born 1997-2012, are less satisfied with their job overall and less likely to stay with their current employer for another two years than other generations. They are also less satisfied with their employee benefits package. Benefits are particularly important to Gen Z: other than higher wages, offering more benefits is the number one action they say their employer can take to best make sure employees are financially secure and well (40% Gen Z vs. 26% Millennials, 22% Gen X, 28% Boomers).

Gen Z’s Financial Priorities: Do They Need Help Now or Later?

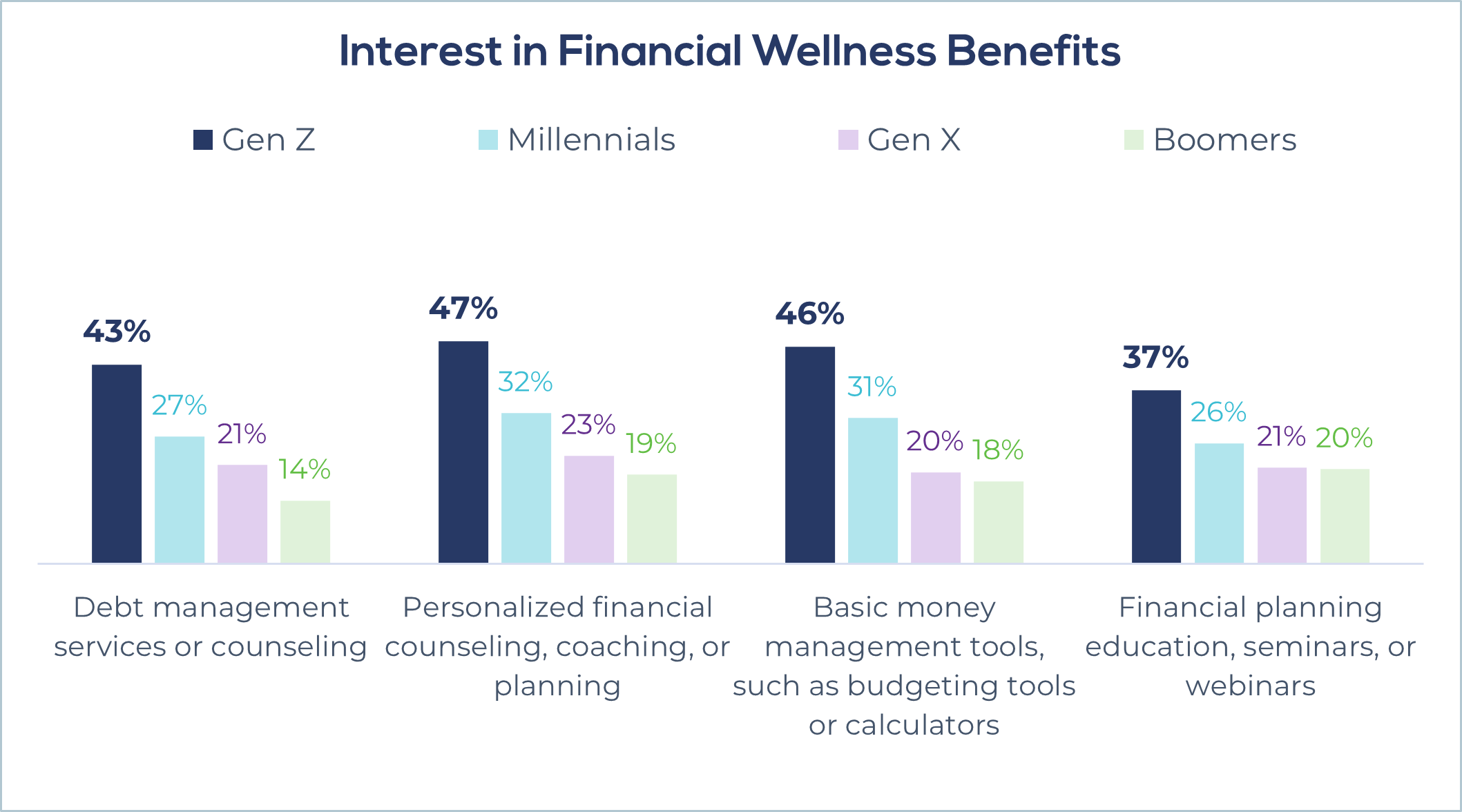

So which benefits are Gen Z workers interested in? Chipotle plans to offer several financial wellness-related benefits, including premium banking to build good credit and a financial wellbeing education platform. These seem to be in line with what Gen Z wants. They express higher interest in a variety of financial wellness benefits, including debt management services, personalized financial counseling, basic money management tools, and financial planning education.

In response to the passing of SECURE 2.0, Chipotle also plans to contribute to a 401(k) retirement savings plan if the employee is paying off their student loans. However, Gen Z cares more about their student loan debt than their retirement savings. When asked to select their current top three financial priorities, more selected student loan repayment than saving enough for retirement (26% vs. 19%). In fact, 44% of Gen Z employees are interested in student loan debt relief/repayment benefits.

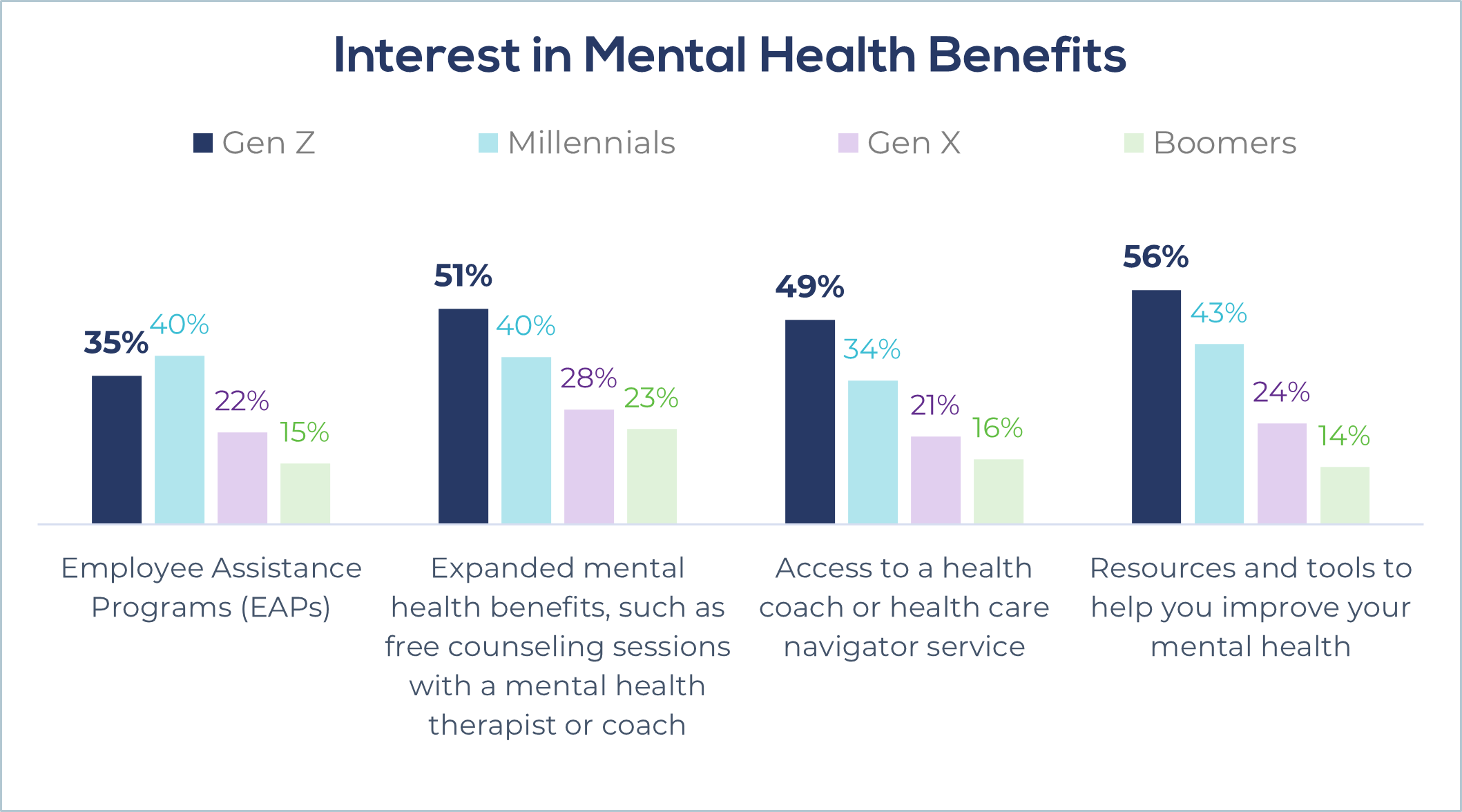

Gen Z’s Focus on Mental Health

In addition to these financial benefits, Chipotle also plans to offer mental health benefits in the form of a new Employee Assistance Program (EAP). Mental health is extremely important to Gen Z. Compared to other generations, Gen Z reports worse emotional well-being/mental health (43% fair/poor vs. 26% Millennials, 20% Gen X, 22% Boomers). They are also more likely than Gen X and Boomers to say their mental health and well-being is negatively impacting their work performance (61% vs. 45% Gen X, 31% Boomers).

Because of this, it’s no surprise that Gen Z expresses more interest in benefits such as EAPs, expanded mental health benefits, access to a health coach, and resources and tools to help improve mental health. While they rate their emotional well-being worse than others, they are open to their employers offering help.

So, did Chipotle get it right? Is their offer the right menu of benefits for Gen Z employees? Financially, Gen Z cares about their money now. They want help managing their finances and paying off their student loans. Retirement savings are less of a priority to them. Gen Z also cares about their mental health.

Gen Z made up just over 1 in 10 of the U.S. workforce in 2023 and is predicted to overtake Boomers in 2024[2]. As they grow in numbers, it’s imperative that employers, like Chipotle, take Gen Z’s needs and wants into consideration when offering benefits.

To learn more about worker well-being, please view the new 2023 Workplace Wellness Report released by Greenwald Research and the Employee Benefit Research Institute (EBRI) or watch Greenwald Research’s coffee break on workplace wellness.

[1] https://newsroom.chipotle.com/2024-01-24-CHIPOTLE-INTRODUCES-NEW-BENEFITS-TO-HELP-ATTRACT-AND-SUPPORT-ITS-GROWING-GEN-Z-WORKFORCE

[2] https://www.glassdoor.com/research/workplace-trends-2024#Trend1